This article was paid for by a contributing third party.More Information.

Transitioning to alternative rates – The countdown is on

The industry has just over two years to begin trading a range of financial products – including loans, floating-rate notes and derivatives products – benchmarked to alternative risk-free rates following the transition away from Libor. Eurex explores how, by being proactive at the earliest opportunity, banks can best manage the burden of preparation ahead of the impending 2021 deadline

The countdown is on to move $350 trillion worth of financial contracts off the beleaguered interest rate benchmark, Libor.

The starting pistol was fired in July 2017, when the chief executive of the UK Financial Conduct Authority (FCA), Andrew Bailey, delivered a speech that stated the regulator would no longer compel the 16 panel banks to submit Libor rates from the end of 2021.

This gave rise to the possibility that banks would stop being contributors for the benchmark and could result in the disappearance of the rate altogether.

It was also the catalyst for international regulators to begin terminating their respective currencies’ Libor.

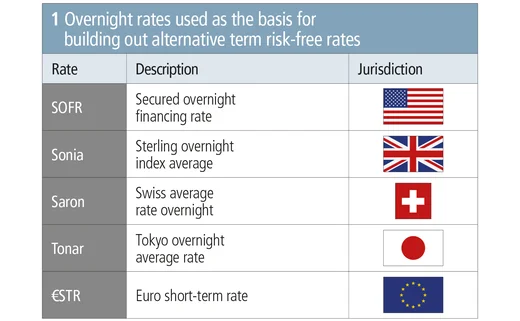

In the European Union – the second largest market behind the US – the industry and regulators have been a little slower on the uptake of the Euribor transition. The European working group, convened by the European Central Bank (ECB), selected the euro short-term rate (€STR) on September 13 last year to replace the euro overnight index average (Eonia), which year-to-date underpins roughly $12 trillion notional outstanding in derivatives contracts.

€STR reflects wholesale euro unsecured overnight borrowing costs of eurozone banks and will be produced by the ECB on October 2, 2019.

That gives the industry just over two years to begin trading a host of financial products benchmarked to the rate, including loans, floating-rate notes and derivatives products.

Readiness

The importance of transitioning to alternative risk-free rates (RFRs) for the industry has seen movement picking up since January for a number of reasons.

In particular, there has been an increase in interest from clients since the beginning of this year. Two events have primarily caused this: first the Dear CEO letter circulated by the FCA and the UK’s Prudential Regulatory Authority in September last year. This began to focus senior individuals’ minds on the need to proceed with this transition.

Second, Brexit has been quite a distraction. Large banks in particular have been forced to relocate staff and businesses to other European hubs, and many firms were caught up in preparation from 2018 into 2019. The Ibor transition was arguably not as high on the agenda as it could have been, given the end-2021 deadline.

From a bank’s perspective – considering that many are working closely with regulators on transitioning away from Ibors – the level of engagement has been at a very senior level within the different organisations.

A focus has spread across both treasury and trading functions to help work out the exposure within each individual bank. Creating an environment committed to communication and organisation around these developments is essential to a successful transition.

Many have warned about not underestimating the scale of the issue, especially considering the amount of work to do with the timeline already on the horizon.

“I think the challenge is the scale at which we need to transition and move away. Now that we have more clarity on the direction and timings, that helps focus the mind from a participant and central counterparty (CCP) perspective,” says Lee Bartholomew, head of fixed income derivatives product research and development at Eurex.

A key area of the market plumbing that will be extremely important in helping derivatives users in particular move away from the old rates are exchanges and CCPs.

Given that many interest rate derivatives are now centrally cleared, and other listed derivatives contracts reference an Ibor, the readiness of industry participants could in many ways be helped by the ability of these firms to take a strong lead in the transition process.

Both LCH.Clearnet and CME Group have made efforts to do this in the US, and Eurex is looking to take up that mantle in Europe.

“In terms of the transition mechanism, we very much want to be a part of that process so the transition is smooth and seamless for customers. I think it affords us an opportunity to develop services around that, and how we can execute that with our members to make sure that transition is smooth,” says Bartholomew.

Challenges in transitioning and building liquidity

All participants agree there will be numerous challenges and stumbling blocks along the way. As €STR will be the last rate produced, Bartholomew says that comes with advantages and disadvantages.

A huge amount of operational work will be completed, such as new systems, new rates, new discount rates and new curves. That Europe may do these things after other jurisdictions could help European constituents learn lessons from other alternative rates that have already had to go through those processes.

“I think Europe has the advantage of hindsight in some respects,” says Bartholomew. “So we can see what has gone on in other jurisdictions – lessons to be learnt – and help factor that in within the working groups. I would say that’s very much underway because participants that are in the working group – and the sub-working groups in Europe – are those that are participating in the other jurisdictions.”

One of the most important factors in helping firms move away from Ibors is if there is a new, deep, liquid market to move to in the first place. Taking into account that new Ibor exposures are still being created all the time, this has been one of the bigger challenges facing the industry to date.

In the UK, the sterling overnight index average (Sonia) market is the most developed. According to weekly data published by the International Swaps and Derivatives Association (Isda), year-to-date US dollar notional volume of Sonia is 56% of sterling Libor. By contrast, equivalent secured overnight financing rate (SOFR) volumes compared to US dollar Libor are less than 0.2%.

Unsurprisingly, because €STR has not yet begun publishing, there is no volume associated with the rate. As a result, participants expect Euribor to be supported for the medium term and, once publication begins, there is an assumption that pressure from regulators will help liquidity move into the €STR-benchmarked market.

A message consistently stressed among market participants to help the Ibor transition has been the need for cash markets to develop for it to be viable for derivatives markets to exist off the back of those products.

It is therefore important to have consistency between the different markets for the hedging strategies to work to help foster the symbiotic growth of both markets.

“The market is focused on getting an ecosystem which is set up and able to handle the vanilla parts of the business, which underpin the banking system,” says Bartholomew. “That includes funding, lending, deposits, and so forth, and then the focus will shift as you build liquidity in those markets, and you have issuance, and you have loans based on the back of them, and then you can then look at the derivatives contracts, and then the more non-linear products, like caps, floors and swaptions.”

The market will also need to familiarise itself and become comforatable with the fundamental differences between the alternative reference rates and the Ibor rates they are intended to replace. The former are overnight rates, while Ibors use term fixings of up to 12 months. Those differences have seen calls for term rates to develop to ease the transition process but, without a robust and liquid derivatives market, that will take time and regulators have been consist in their recommendation that this should not be relied upon.

Despite these teething problems, progress is being made. A cross-currency swap between SOFR and Euribor was made recently while the floating rate note market has been the quickest to issue bonds linked to the alternative rates among cash products.

“It’s something that the market is grappling with,” says Bartholomew. “I think, as you start to see issuance pick up and move further, the market can then start to build out further in terms of the term component, but I think it’s a combination of inputs – with not one more important than the other – in order to establish a liquid market.”

Role of exchanges and CCPs

Given the eurozone is further behind in the timeline of developing alternative rates, the role of key infrastructures in the marketplace such as exchanges and CCPs could, in theory, be dampened for now, but Eurex’s Bartholomew does not think so.

When Euribor might disappear is well known based on the end of 2021 deadline, which means firms must get busy preparing despite an €STR rate not yet existing.

“From an exchange perspective I would say that we, like all the other members of the working groups, have certainly put a great emphasis on ensuring we are able to service our members when the dates arrive, and make sure that we’re ready from that perspective,” he says.

A move to align Europe’s progress with what is happening elsewhere is widely considered the correct approach. Part of that alignment is trying to make the shift away from Europe’s current unsecured RFR, Eonia, as well as Euribor. Currently, the plan is to recalibrate Eonia so it functions at €STR plus a spread, which Bartholomew agrees is the best approach for the smooth functioning of the market.

“I think we’re bound to hit some speed bumps, but the market will focus its attention – and is focusing its attention – on looking to make the new RFRs a success. So I belive it is the best approach to take,” says Bartholomew.

Once €STR is published, the key role of exchanges and CCPs such as Eurex will be offering products to help build liquidity in derivatives based on the new rate – be it in over-the-counter or listed markets. Bartholomew anticipates Eurex being quick to market after the beginning of the rate publication.

One of the easiest ways for firms to shift to the new rate is via a protocol mechanism, of which Isda has been at the forefront since the new alternative rates were established. For SOFR, Sonia, the Swiss average rate overnight (Saron) and the Tokyo overnight average rate (Tonar), Isda hopes for those protocols to be ready by the end of the year, and CCPs such as LCH and CME have already agreed to help shift contracts cleared at those firms away from the respective Ibors and to new rates.

In the eurozone, this will be possible once legal fallback language is established for Euribor contracts.

“I think people will embed it as a protocol and, once we have clarity on the fallback language, it will be widely adopted. But it has to be seen that it’s balanced,” says Bartholomew.

“One thing you want to avoid is people putting it off and then, at the last minute, everybody running for the door to try and get it done. I think if you can be proactive now in doing it then it helps facilitate the market as well, on a broader perspective, but you’ve got to assess that for your own portfolio and then act accordingly,” he adds.

Sponsored content

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@risk.net

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@risk.net