Achieving portfolio transparency with AMCs

Actively managed certificates (AMCs) are set to take off in Asia as family investors look for portfolio visibility

Amid the uncertainty and market volatility brought by the Covid‑19 pandemic this year, now is a good time for investors to be taking stock of asset allocations in their portfolios.

For Asia’s private wealth holders and family offices, the problem is that assets are often scattered across different markets and locations, making it tricky to get a quick grasp on what is in their portfolios overall.

This predicament is now driving growing numbers of external asset managers (EAMs) and family offices across Asia to turn to AMCs, says Tan Yew Kiat, executive director of derivatives sales for Asia‑Pacific in the global markets team at UBS.

With AMCs, investors can get complete transparency with visualised detail of their portfolios, along with live updates and detailed reports on the performance and valuations of their asset allocations.

“That’s why we have seen a significant pickup in interest from clients in consolidating assets into a central, convenient instrument whereby they can look at risk, performance and so on in one place,” he says. “During [February and March], when markets were moving really fast, they came to the realisation that it was important to have that kind of oversight.”

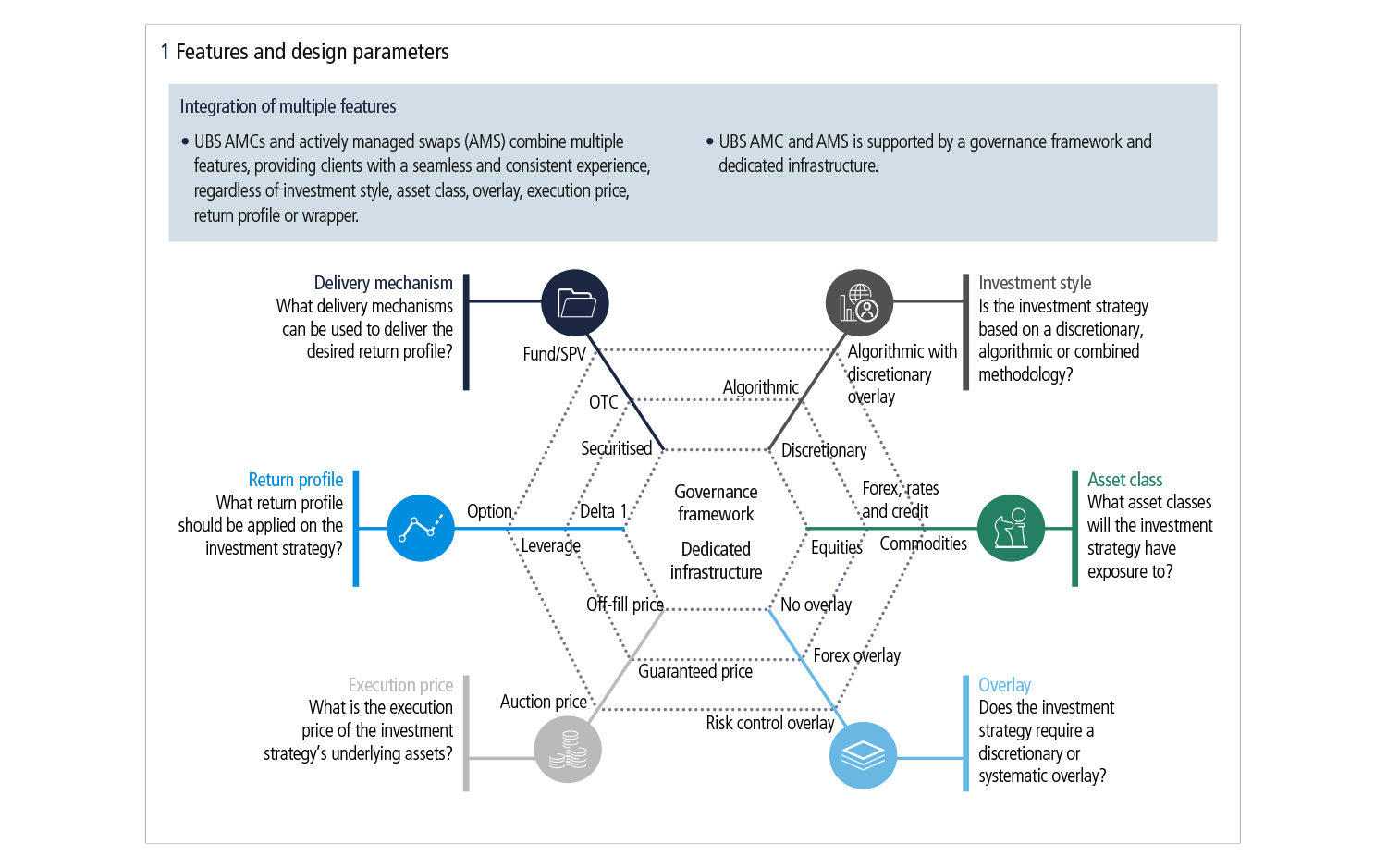

They are typically issued by investment banks or their special purpose vehicles (SPVs) and tend to be targeted towards clients such as private banks, high-net-worth individuals, as well as family office EAMs. AMCs are still relatively new in Asia, but are already well established in Europe.

Investing in AMCs leaves portfolio managers free to focus on their core competency – asset allocations – while the issuer takes care of the implementation, execution and delivery of the chosen investment strategy.

With investors in the region now looking

for greater flexibility, cost efficiency and transparency around the management of their portfolios, AMCs are starting to turn a lot of heads, says Tan.

Advantages of AMCs

One investment firm in the region that has recently discovered the advantages of AMCs is Singapore-based Straits Investment Management (SIM). The firm started off managing capital for Straits Trading Company, but in October last year began accepting managing capital for external clients.

It was at this time that SIM launched its first AMC, issued by UBS. Since AMCs are unitised, they make it easier to manage the numerous portfolios of different families or individual investors.

“We started accepting money from third parties – and that’s where our AMC has added a lot of value,” says Manish Bhargava, SIM’s chief executive. “Because it’s working so well, we’re thinking of doing another.”

“AMCs allow you to make easy use of derivatives for portfolio overlays and hedges, or different thematic strategies such as an investment basket focused on the working from home theme”

Lawrence Lee, Sino Suisse

The certificate, Straits Global Property, is an absolute return strategy that invests primarily in equities. With signs of frothiness in global equity markets becoming more evident last year, SIM wanted a strategy geared to delivering positive returns both when markets are going up and when they are going down.

Like a lot of investors at the time, Bhargava felt that the top of an ageing bull market was approaching.

“You can’t go naked long in this market,” says Bhargava. “[The AMC] is also operationally very light and provides a nice consolidated report so investors can easily see where their portfolio stands.”

The strategy adopted by SIM proved to be a smart choice: the AMC was up 3.1% (net of fees) year-to-date, as of the end of August. In comparison, the Global Property Index was down 16.6% at the same time.

As Asia’s family offices are now beginning to discover, AMCs also have a host of other beneficial characteristics. A rapid time-to-market of the issuing process is one such characteristic that would have proved invaluable when market sentiment began to turn after the market selloffs at the start of the year.

For SIM, it took roughly a month to get its AMC up and running – but the process can be even quicker. It can take just a week to set up an AMC for existing clients, says Tan at UBS. Consequently, a client that decided to launch a product in late March was still able to capture much of the rally in the next quarter after the Covid‑19 crash, he adds.

Others, such as Eric Pong, founder of Avenue Family Office, a Hong Kong-based EAM, point to the relatively low cost of AMC solutions as the key benefit. The issuing bank, in this case also UBS, takes care of all the administration and auditing, saving on the cost of setting up a fund structure, he says.

Pong also cites the sophistication of UBS’s AMC Neo platform as an additional benefit. Furthermore, with their “very good reputation and credit rating, we don’t need to worry about issuer risk,” he says.

Currently, Avenue is using the AMC predominantly for investing in Hong Kong, UK and US stocks. But, like SIM, the firm is now weighing up the launch of a second certificate in the near future with the aim of investing in different types of underlying assets, such as fixed income assets.

Sino Suisse, a Singapore-based EAM, is also considering using AMCs for its clients in the near future, says chief investment officer Lawrence Lee. The firm would be looking to set up a multi-asset vehicle that invests in both equities and fixed income assets. Lee says that he likes the products’ convenience, transparency, flexibility and the range of underlying assets and strategies on offer.

“AMCs allow you to make easy use of derivatives for portfolio overlays and hedges, or different thematic strategies such as an investment basket focused on the working from home theme,” he says.

Another potentially big and relatively untapped source of demand for AMCs is family wealth in India, where the solutions are not typically available onshore, says Munish Randev, founder of Cervin Family Office in Mumbai. “We have simpler cousins, like equity-linked debentures – simple principal-protected products.”

Some sophisticated offshore Indian family offices have invested in AMCs, but in-country demand has been insufficient to result in large enough syndicated commitments to international private banks, Randev says. He believes that may be set to change.

“Wealthy Indians and families have steadily increased their investment into overseas assets – they have realised they need to create a more active international portfolio,” he says.

“Ultimately, if a bank can offer a solution for overseas investment that’s efficient and simple and can give the exposure we’re looking for, that’s great. Clients sending money out of India want to take it step-by-step and increase the amount over time as they become more comfortable with the offshore allocations.”

What is clear is that, across Asia, the, transparency, simplicity, flexibility and cost-efficiency offered by AMCs is starting to catch the attention of EAMs and some family offices too.

With the market uncertainty created by the Covid‑19 still showing little sign of abating, Tan says growing interest in AMCs among these client segments in the region looks like it is only just getting started.

“We are still in the nascent stages of discussing AMCs with family offices in Asia, but 2020 has seen the fastest adoption so far,” he says. “The take-up rate is pretty high in the EAM segment, and I think we’ll see it increase among family offices in the near future.”

Family office investing – Special report 2020

Read more

Sponsored content

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@risk.net

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@risk.net