Monthly swaps data review: ADV for OTC derivatives

Daily volumes are a pillar of the futures market, and can now be found for US swaps

Average daily volume (ADV) is one of the listed derivatives market’s statistical pillars. Published by exchanges for each of their contracts, it is widely used by participants as a way to compare market sizes and decide trading strategies.

An analogous figure can now be derived from over-the-counter market data. As in the futures market, ADV for swaps could allow investors and hedgers to work out where they are best able to execute – and may also have the added benefit of encouraging futures market-makers to take a fresh look at the opportunities of expanding into the OTC space.

The caveat is that notional figures, arguably the simplest and most appealing way of comparing OTC trading volumes, are also the wrong starting point – sensitivity to interest rates is a better basis for comparison.

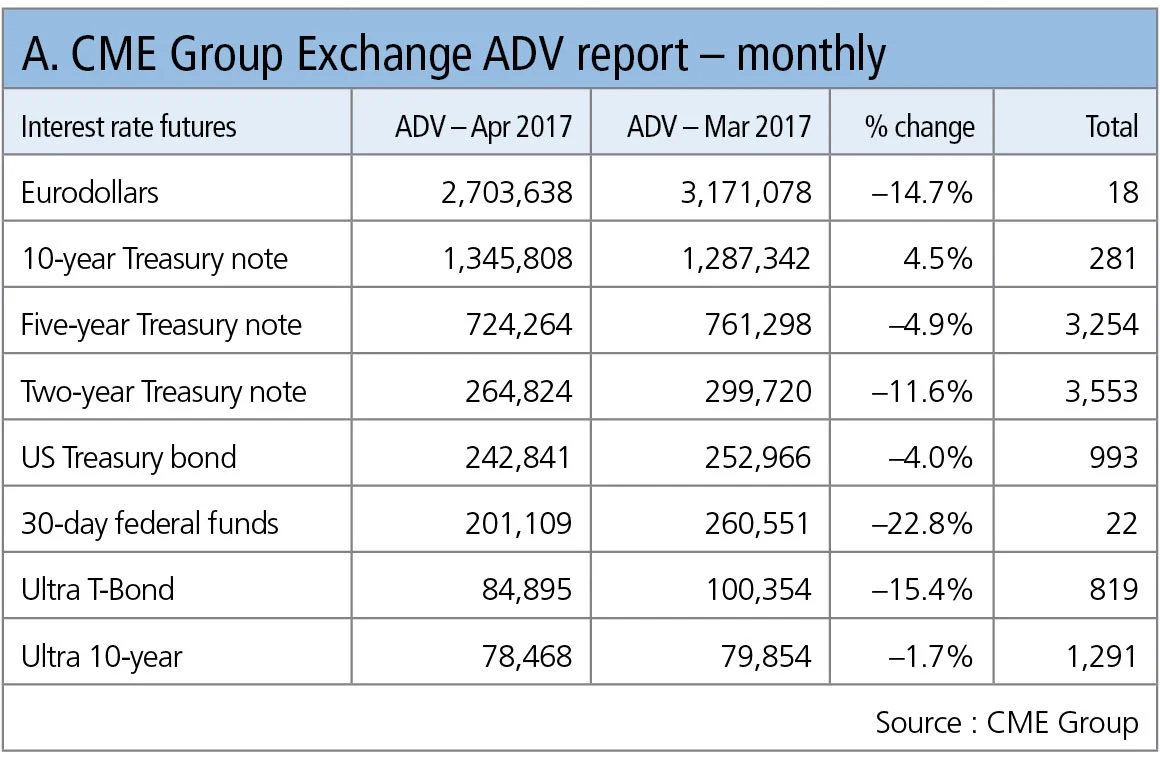

As an example of ADV disclosures in the listed market, the table below – taken from a CME Group report – shows ADV data for April and March 2017.

Table A shows:

- ADV as the number of contracts traded for each market, with Eurodollars the largest, with 2.7 million in April, down 14.7% from March.

- The 10-year Treasury note is next – and so it continues in declining order of volume, with the data showing April trading was lighter across the board, particularly for the federal funds and Eurodollar contracts, with only the 10-year Treasury note higher.

- Note some of these markets have different contract sizes, for example Eurodollar is $1 million per contract while the 10-year Treasury note is $100,000.

US dollar interest rate swaps

One impact of the Dodd-Frank Act in the US has been the public dissemination of trade-level data for OTC derivatives and the granular transparency this provides makes it possible to calculate ADV for specific products in an analogous fashion to futures.

By filtering and categorising the public dissemination record, it is possible to calculate ADV for specific products.

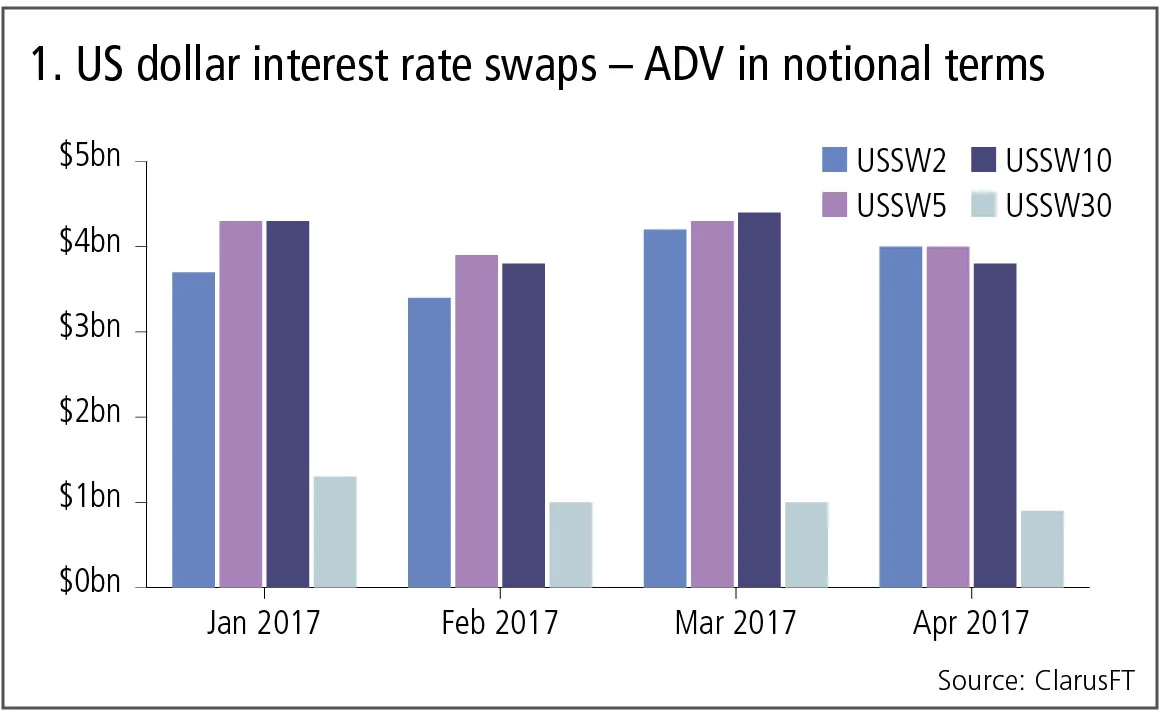

Figure 1 shows:

- ADV for the major vanilla US dollar swaps, denoted by their commonly used Bloomberg tickers of USSW2, USSW5, USSW10, USSW30, with the number corresponding to the maturity in years.

- The two-year, five-year and 10-year swaps each show approximately $4 billion ADV.

- The 30-year product has approximately $1 billion ADV.

This chart highlights the importance of the unit selected for ADV and while notional is useful to compare a specific ticker over the months in question, it is less useful when making comparisons between these tickers as the risk of a $100 million five-year swap is roughly half that of a 10-year swap.

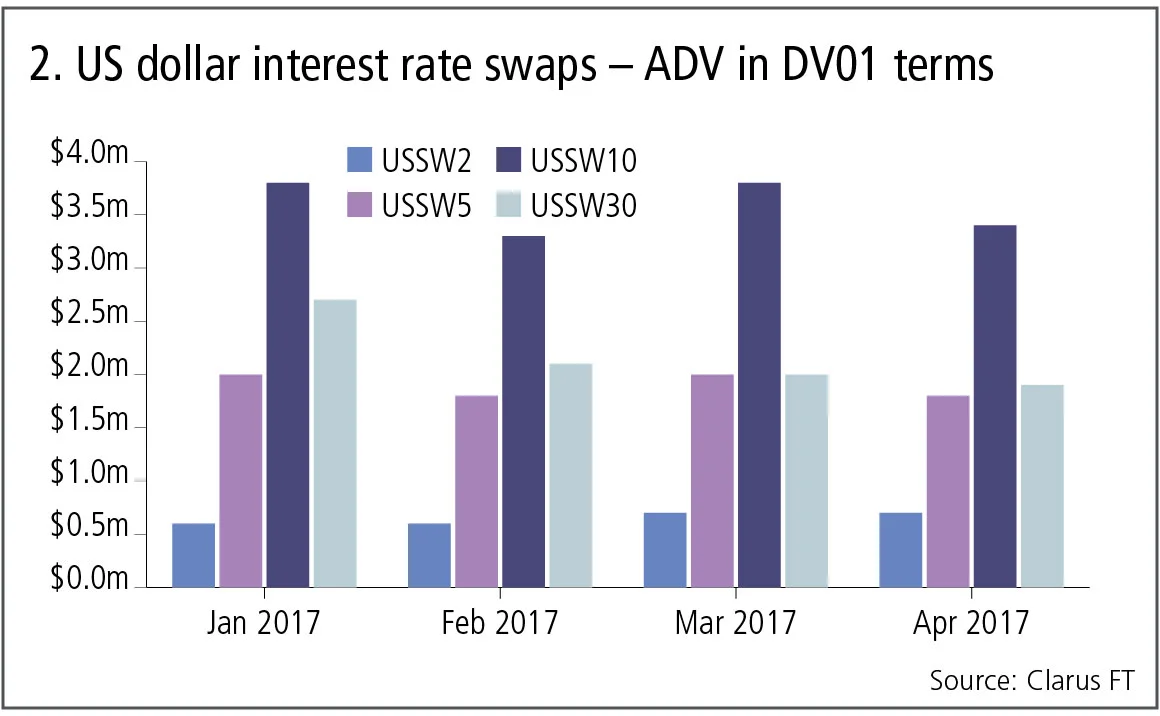

Calculating ADV using the per-basis point interest rate sensitivity – DV01 – gives a different picture.

Figure 2 shows:

- USSW10 is the largest, with $3.4 million ADV in April 2017, which is down 13% from $3.8 million ADV in March 2017.

- USSW30 is the next largest, with $1.9 million ADV in April, down 6% month-on-month.

- USSW2 is the lowest, with $0.7 million ADV in April.

- Volumes in April are lower than March, similar to the CME figures above.

Caveats and assumptions

These ADV figures are not perfect and like any measure it is important to understand the assumptions before using.

First, US public dissemination rules mean that for trades above specified notional sizes – by asset class and tenor – the full notional is not disclosed. For instance, a 10-year interest rate swap would show as $170 million, whether the notional was $175 million or $250 million. In practice, this can understate the ADV by 20–30%.

Second, this is not global ADV for USSW30, it is the liquidity in the US market only. This is different to a futures contract where global liquidity is typically concentrated at the single exchange where the product trades.

Until Europe and Asia provide more public dissemination of OTC derivatives data, what we have are US ADVs, representing approximately 45% of global ADV for these instruments. More data will be available following the arrival next year of Europe’s new trading and transparency regime – the second Markets in Financial Instruments Directive (Mifid II).

US dollar overnight indexed swaps

Let’s turn now to the fed funds index and US dollar swaps that reference the overnight indexed swap (OIS) rate.

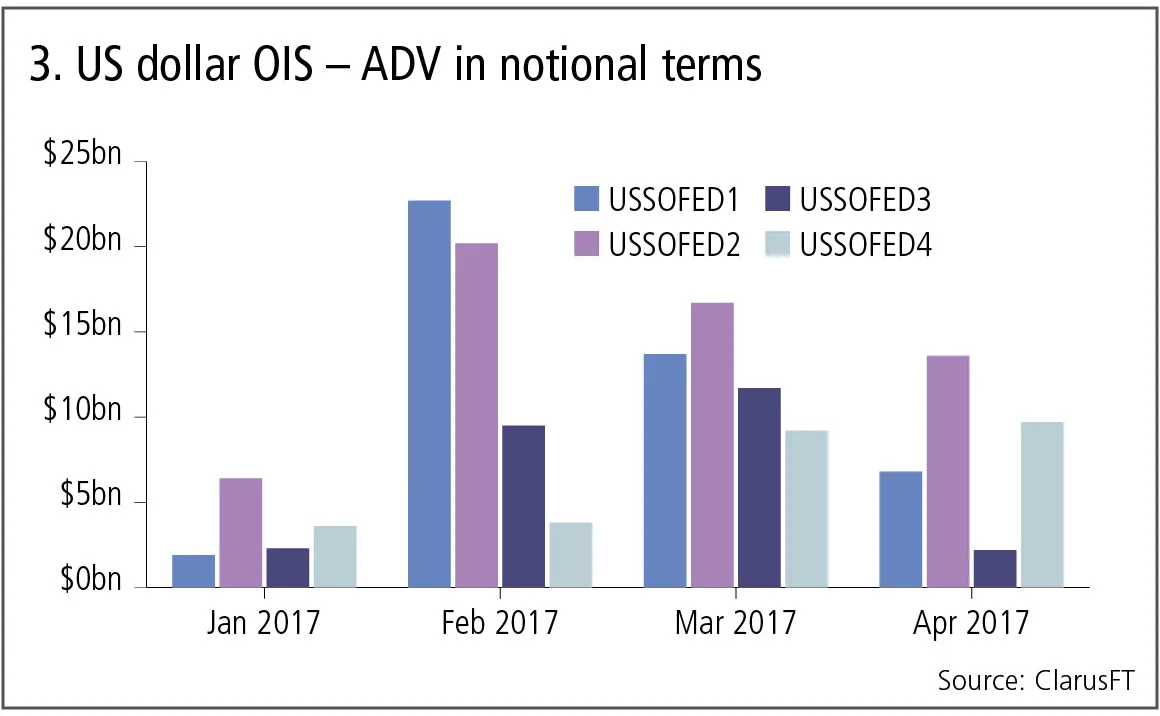

Figure 3 shows:

- The most common US dollar OIS swaps correspond with meeting dates for the Federal Reserve’s rate-setting committee, so USSOFED1 has a start date of the next meeting and a maturity of the subsequent meeting.

- As the meetings are generally six weeks apart, each of these represent short-dated swaps, making large notionals the norm.

- Feb 2017 shows a huge spike in volumes of FED1 and FED2, previously highlighted by this column.

- These subsequently dropped in March and again in April.

- April volumes are back down from their high, but remain well above January, only FED3 – the July 26 to September 20 period – showing low volume.

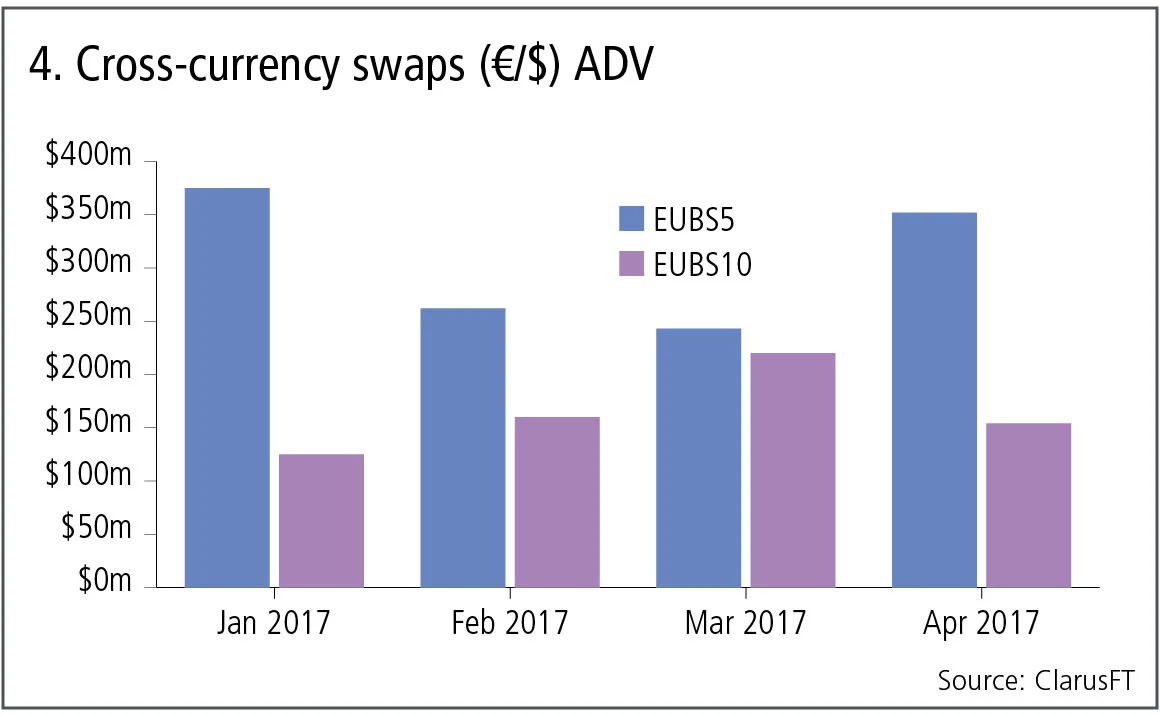

Cross-currency swaps

Cross-currency swaps are one of the largest products covered by non-cleared margin rules.

Figure 4 shows:

- €/$U cross-currency swaps, EUBS5 and EUBS10.

- EUBS5 ADV in April is €350 million ($391 million), up 45% from the €243 million in March and just below the high of €375 million in January.

- EUBS10 ADV in April is €154 million, down 30% from the €220 million in March.

Other jurisdictions

Aside from the US, Canada is the only other jurisdiction with trade-level public dissemination from trade repositories, which is required for the above analysis.

While Europe, Japan and other jurisdictions have daily transaction reporting to trade repositories, none have trade-level public dissemination. The only public reports available are at such a high level of aggregation that they are entirely useless to market participants: a missed opportunity to add transparency to these markets and complete the global picture.

Mifid II will provide much more useful data. The only caveat is that the complexity of regulations that seek to cover securities, exchange-traded and OTC derivatives means there is an over-reliance on unique identifiers, whch will make real-world use by market participants unnecessarily difficult.

Only users who have a paid subscription or are part of a corporate subscription are able to print or copy content.

To access these options, along with all other subscription benefits, please contact info@risk.net or view our subscription options here: http://subscriptions.risk.net/subscribe

You are currently unable to print this content. Please contact info@risk.net to find out more.

You are currently unable to copy this content. Please contact info@risk.net to find out more.

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@risk.net

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@risk.net

More on Comment

G-Sib capital surcharge: how indexing and averaging alter incentives

Capital risk strategist anticipates Basel III endgame impact on US big-bank behaviour

Podcast: Abi-Jaber and Li on a ‘sticky’ volatility problem

The pair discuss their model to jointly capture Vix, SPX and SSR

Markets perceive the future in very distorted ways

Discounting paradigms should adapt to be more realistic, says Jean-Philippe Bouchaud

Op risk data: Cyber hacks shake crypto protocols

Also: JP Morgan fined over investor losses; Symetra’s Methodist pensions mess. Data by ORX News

Prediction markets can be a canary in the coal mine

Prices of contracts on the likes of Polymarket can act as signals for risk management and hedging, says risk expert

How AI agents can join the dots for risk managers

Citi risk expert outlines agentic AI tool that would pull together structured and unstructured data on trading and lending approvals to create single, unified view of risk

Op risk data: Corporate spies spell trouble for BBVA

Also: BofA buttonholed for alleged Epstein links; minority shareholders take a bite of Brookfield. Data by ORX News

The rise of AI politics

AI should not be treated as just another technology, writes MAS adviser David Hardoon