Monthly swaps data review: ETD vs OTC margin totals

New disclosures from big CCPs show listed market consumes more margin than cleared swaps

It sometimes seems a point of pride for over-the-counter market participants that their trades are so chunky in risk terms, with longer-dated interest rate swap transactions, for example, sometimes transferring more than a million dollars in per-basis point exposure.

But how much risk exists in the OTC market as a whole? A fresh batch of disclosures from central counterparties (CCPs) helps answer that question – at least for the cleared portion of the market. Summing the total amount of initial margin (IM) collected by the big four derivatives CCPs produces a total of $171 billion. That’s less than the $191 billion in IM the same clearing houses collectively hold for their exchange-traded derivatives (ETD) – so while the OTC market might have bragging rights in terms of the amount of risk transferred per ticket, it seems like the ETD market represents the larger pool of risk as a whole.

In other news, March was another big month for the US dollar overnight indexed swap (OIS) market – which appears to be growing in popularity as US rates rise – and particularly for TrueEX with roll volume of just over $3 trillion in the month. That represents almost two-thirds of the total OIS volume executed on swap execution facilities (Sefs) in March.

CCP quantitative disclosures

On a quarterly basis, central counterparties make disclosures in over two hundred quantitative data fields – covering collateral, credit risk, default resources, liquidity risk, margin and more – a voluntary initiative of the Committee on Payment and Market Infrastructures and the International Organization of Securities Commissions.

This data permits the analysis of quarterly trends at individual CCPs, or the comparison of different venues.

One topic on which the data sheds new light is the relative size of exchange-traded and OTC derivatives markets, thanks to the publication of IM numbers – the amount of funds a CCP requires from its clearing members to cover the risk of their positions.

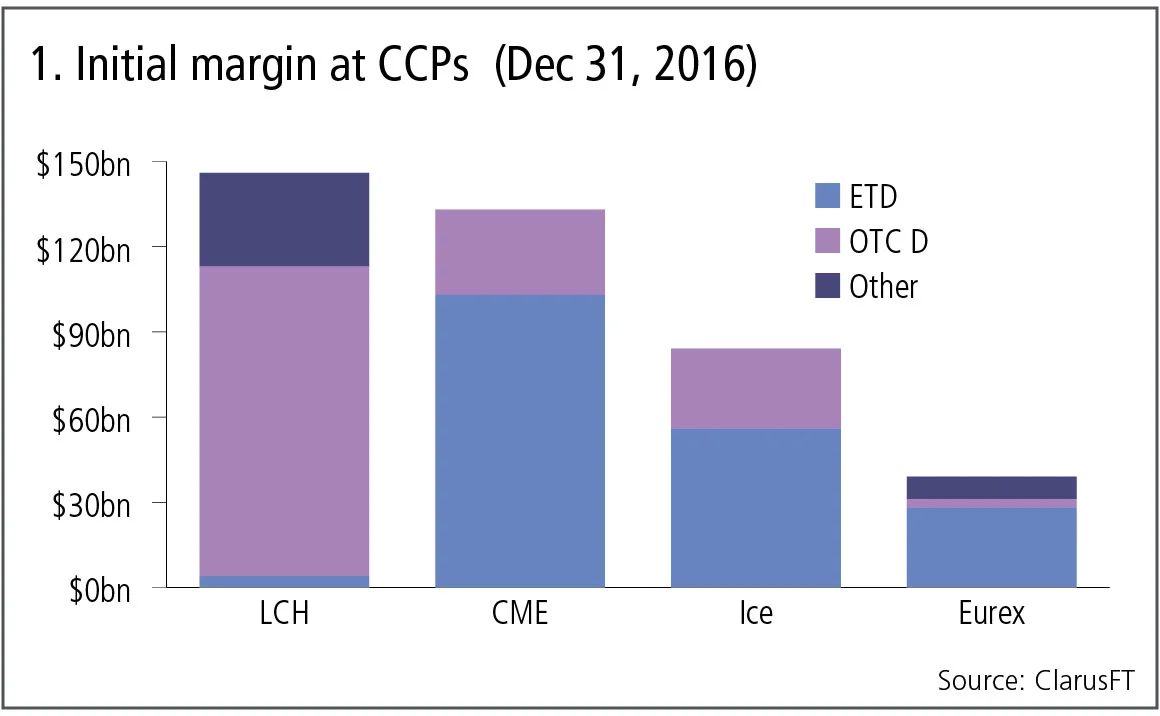

Figure 1 shows:

- LCH with $147 billion of IM, of which the largest is OTC at $109 billion, followed by ‘other’ – covering its fixed income, repo and equity clearing services – at $33 billion.

- CME with $133 billion of IM, of which the largest is exchange-traded derivatives (ETD) with $103 billion, followed by OTC derivatives at $30 billion.

- Ice with $84 billion of IM, of which ETD is $56 billion and OTC is $28 billion.

- Eurex with $38 billion of IM, of which ETD is $28 billion, OTC is $3 billion and ‘other’ is $8 billion.

Summing the ETD and OTC figures from above shows the former with a total of $191 billion in IM versus $171 billion. This tells us not only that the exchange-traded market is larger than the cleared OTC market in margin terms, but also in risk terms. Why? Because ETD is typically margined over a one-day or two-day holding period, while OTC products face a five-day period; a comparable ETD margin over five days would be higher by approximately 1.5 to two times.

Dealer vs client

An interesting difference between ETD and OTC markets is that client margin in the former is generally larger than dealer margin – also known as ‘house’ margin – primarily because there are many more clients than dealers, with the clients typically holding more directional portfolio exposures than the dealers’ flatter market-making books.

At CME, for example, client initial margin for ETD is 86% versus 14% for house IM.

This split is very different for OTC derivatives as dealers have been clearing for more than a decade, while client clearing in swaps only started a few years ago and has yet to become mandatory for the majority of clients.

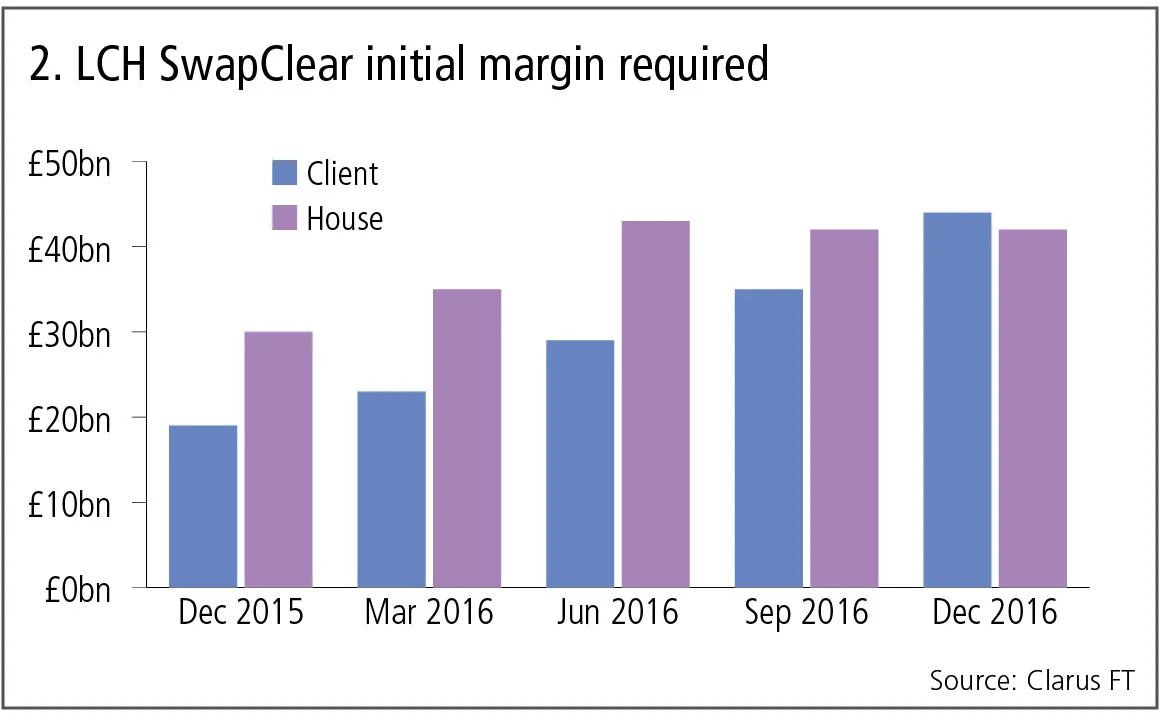

LCH figures for its SwapClear service illustrate this.

Figure 2 shows:

- Client IM exceeding house IM for the first time in the latest quarter.

- House IM growth levelling off after June 30, 2016.

- Client IM growing 135% over the one-year period, compared to 40% for house IM over the same span.

- For the six months from the end of December 2015 to the end of June 2016, the client IM share was 40%. This has jumped to 51% in the latest quarter.

US dollar swaps

Talking of growth, March 2017 was a significant month for volumes, with record highs for a number of interest rate products, such as CME’s interest rate futures. For US dollar swaps, volume figures can be compiled from the various US Sefs.

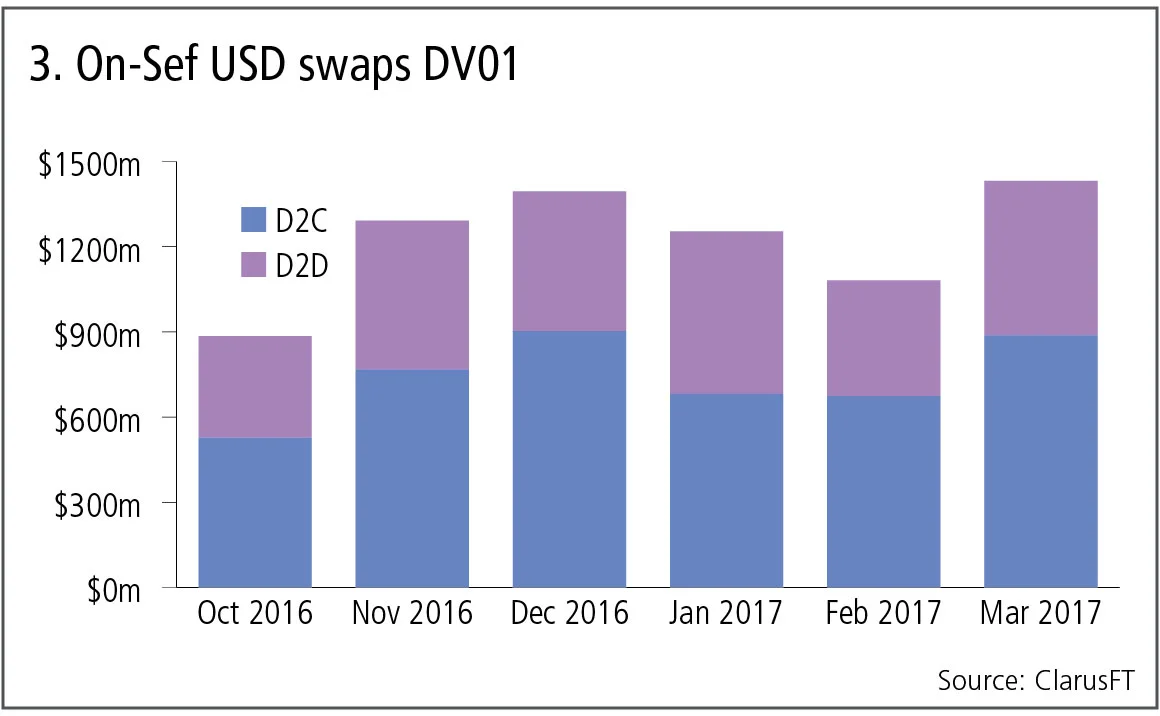

Figure 3 shows:

- March 2017 is the highest month on record with $544 million in DV01 – the sensitivity to a one-basis point move in rates – traded at dealer-to-dealer Sefs and $888 million at dealer-to-client Sefs, a total of $1.4 billion DV01.

- That exceeds the previous high in December 2016 by 3%.

- In gross notional terms, March volume was $2.8 trillion.

- Both March and December saw the Federal Reserve raise rates.

- And these two quarters are significantly up on earlier periods in 2016.

US dollar OIS

Last month’s article revealed a massive increase in February volumes for US dollar-denominated overnight indexed swaps, both on- and off-Sef. March saw another big jump, with some eye-catching figures at individual Sefs.

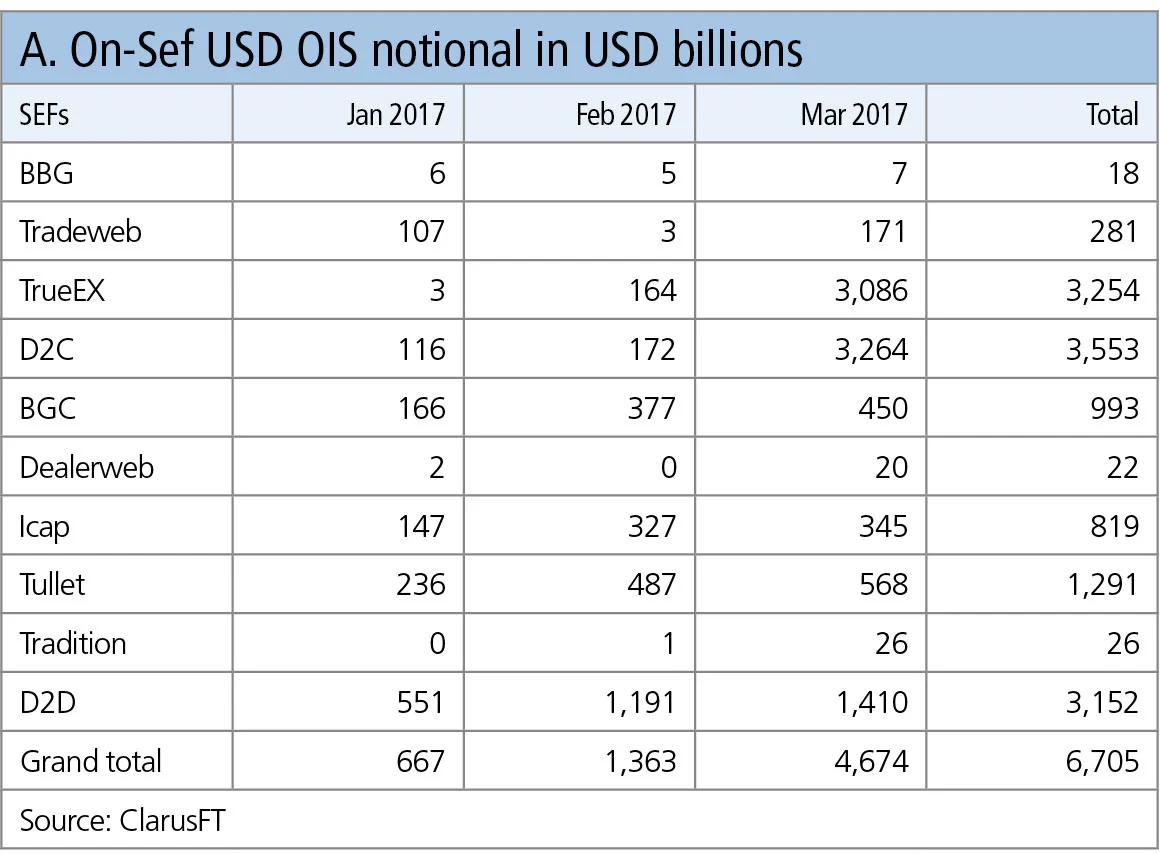

Table A shows:

- A massive increase to $4.67 trillion in March 2017.

- TrueEX alone executed a stunning $3 trillion.

- Having differentiated itself successfully with portfolio maintenance services, such as package compression and allocation, TrueEX now appears to be doing the same with rollover volume from one Federal Reserve meeting date to another.

- Dealer-to-dealer Sefs also up to $1.4 trillion from $1.2 trillion, with Tullett the largest at $570 billion, followed by BGC at $450 billion.

US swap data repository (SDR) numbers show off-Sef volume for US dollar OISs in March is up from the prior month and greater than $2.6 trillion; how much greater is not disclosed by SDR data, but it could be as large or larger than the $4.7 trillion in gross notional that was executed on-Sef.

Non-cleared margin and cleared volumes

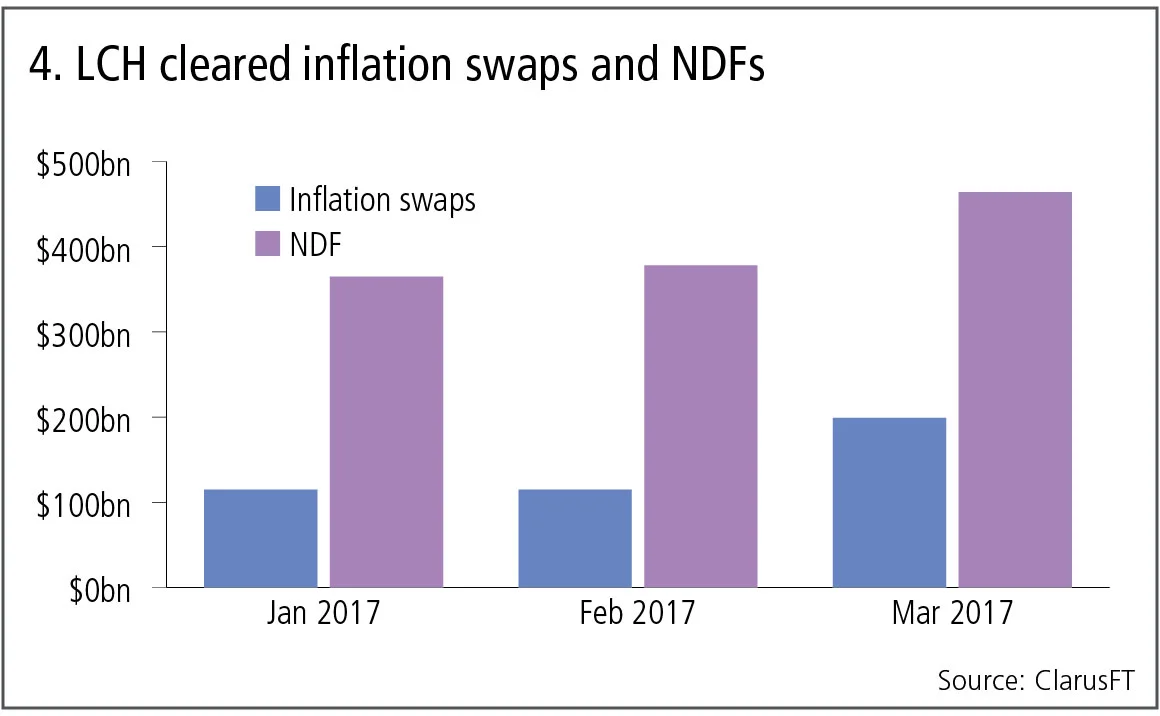

Last month’s article also looked at the impact of non-cleared margin rules on the volumes of selected cleared products. It’s worth updating this for cleared inflation swaps and non-deliverable forwards (NDFs) at LCH, where volumes have continued climbing.

Figure 4 shows:

- Big increases for both products.

- Inflation swaps up by 72% to $199 billion.

- NDFs up by 23% to $464 billion.

It will be interesting to see how much more cleared volumes can increase in these products – there could be a lot of growth to come, as client clearing is only just getting off the ground.

Only users who have a paid subscription or are part of a corporate subscription are able to print or copy content.

To access these options, along with all other subscription benefits, please contact info@risk.net or view our subscription options here: http://subscriptions.risk.net/subscribe

You are currently unable to print this content. Please contact info@risk.net to find out more.

You are currently unable to copy this content. Please contact info@risk.net to find out more.

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@risk.net

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@risk.net

More on Comment

Markets perceive the future in very distorted ways

Discounting paradigms should adapt to be more realistic, says Jean-Philippe Bouchaud

Op risk data: Cyber hacks shake crypto protocols

Also: JP Morgan fined over investor losses; Symetra’s Methodist pensions mess. Data by ORX News

Prediction markets can be a canary in the coal mine

Prices of contracts on the likes of Polymarket can act as signals for risk management and hedging, says risk expert

How AI agents can join the dots for risk managers

Citi risk expert outlines agentic AI tool that would pull together structured and unstructured data on trading and lending approvals to create single, unified view of risk

Op risk data: Corporate spies spell trouble for BBVA

Also: BofA buttonholed for alleged Epstein links; minority shareholders take a bite of Brookfield. Data by ORX News

The rise of AI politics

AI should not be treated as just another technology, writes MAS adviser David Hardoon

AI risk management and the shift to capability control

By reframing validation, banks can align innovation with regulatory demands and maintain robust risk discipline, argues risk manager

Tokenised commodities could help oil the machine

Shifting physical assets onto the blockchain eases collateral frictions, argues crypto expert