Technical paper/Technology

Trading strategies via book imbalance

Predicting equity and futures tick by tick price movements

Improving annuity pricing with address data

Technical papers

Inflation ist normal

Der Neueste Stand - Inflationsderivate

Valuation and risk analysis for Dutch pension schemes

Technical papers

Das Kontrahentenrisiko und CCDSs unter Korrelation

Der Neueste Stand - Hybrid-Risiko

Copule archimediane implicite nei dati di mercato

Approfondimenti. Derivati creditizi

Contributi al rischio di fattori generici definiti dall'utente

Approfondimenti - Gestione degli investimenti

Calibrazione di tranche CDO con il modello dinamico GPL

Approfondimenti - Derivati di credito

Modelling South African swap spreads

Sponsored Statement

Kalibrierung - Markov-Projektion zur Kalibrierung der Volatilität

Der Neueste Stand

Expected shortfall - una coda in due parti

APPROFONDIMENTI. RISCHIO DEL PORTAFOGLIO CREDITI

Sorridere alle convessità

Approfondimenti. Volatilità implicita

Iterating cancellable snowballs and related exotics

Cutting edge: Exotic options

Strategie di trading sulla pendenza

DERIVATI CREDITIZI

Counterparty risk - Wrong-way risk modelling

Cutting edge

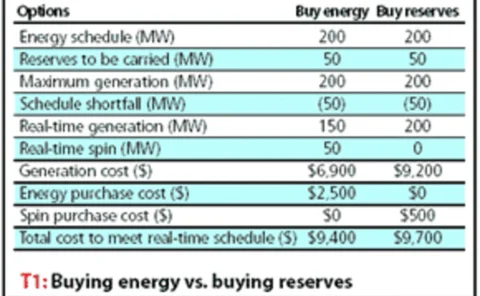

At the flick of a switch

Jesper Andreasen and Martin Dahlgren present a regime-switching model for electricity derivatives that incorporates spiky spot-price dynamics and allows for closed-form pricing of forwards, options and swaptions

Nuclear fusion R&D

In 50 years, nuclear fusion may be a major source of energy, but until then extensive research and development is needed. To justify the current and future R&D expenditure, a cost-benefit analysis designed specially for this sector is required. David…

A matter of principal

Developing term structure models can be tricky, as unknown factors and non-observable variables can affect futures prices. But principal components analysis is useful in tackling these problems. Here, Delphine Lautier uses PCA to pin down price movements…

Bond execution models

Quantitative trading l Cutting edge

Real-time trading

Rankings 2005