Basel Committee

Moody's unveils default loss model

Credit tech

The Basle II capital accord: op risk proposals in brief

BASLE II UPDATE

UK firms face increasing op risk

ASSET MANAGEMENT

AIB loss poses questions for the banking industry

FRONT PAGE NEWS

Regulators concentrate on key op risk issues for QIS3

FRONT PAGE NEWS

Basle regulators still hope for 2005 date as doubts increase

BASLE II UPDATE

Basle II delay could help EU

BASLE II UPDATE

On the road to Basle III

INSURANCE COMPANIES

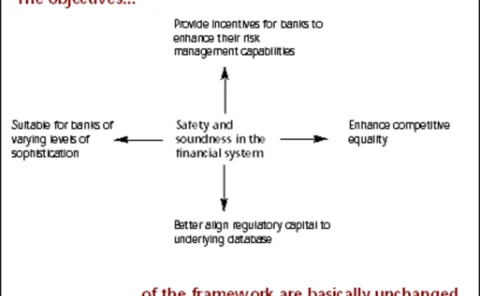

Regulator hits back at Basle II critics

BASLE II UPDATE

Moody's launches LossCalc

Moody’s Risk Management Services (MRMS) claims that its latest product, LossCalc, is the first risk management tool to predict loss-given default (LGD) for investors in the event of a company’s bankruptcy.

Regulation | On the road to Basel III

UK regulators want to harmonise regulation of the financial services sector – and they have insurance companies in their sights.

Basel II final paper delayed until 2003

Global banking regulators now expect to issue their final version of the complex and controversial Basel II bank capital adequacy accord “some time next year” rather than by the end of this year as previously hoped.

Survey delay puts Basel II timetable under further strain

Delays in issuing a crucial survey could again imperil the timetable of the Basel II bank capital adequacy Accord and further endanger the European Commission’s schedule for risk-based bank regulation.

Dealing with the flak

With the final Basel Accord proposals due to be published later this year, the Bank of International Settlements’ new Asian head, Shinichi Yoshikuni, does not have much time to settle into his new role, writes Nick Sawyer.

Weary recognition of gross income as Basel II op risk measure

LONDON - There was "weary recognition" among bankers that the use of gross income as a measure of operational risk was the least bad approach, said Richard Metcalfe, co-head of the European office of the International Swaps and Derivatives Association …

Retail banking accounts for two-thirds of op loss events, says Basel survey

BASEL, SWITZERLAND -- Operational losses in retail banking accounted for two-thirds of the number of operational losses suffered by banks, according to a survey by global banking regulators. The survey sought data about the impact on major banks of the…

The Basle II capital accord: op risk proposals in brief

This summary has been updated to include the revisions to the Basle II op risk proposals contained in the Working Paper on the Regulatory Treatment of Operational Risk issued in September, 2001 and available on the Bank for International Settlements’…

UK regulators ponder op risk charge for insurers

LONDON -- British regulators are deciding whether to impose a specific capital charge on insurance companies for operational risk under new risk-based rules aimed at making the UK insurance industry safer.

Loss survey supports arguments against capital charges, say fund managers

London - The results of a survey by global banking regulators of banks’ operational loss experience support arguments against using capital charges as the main protection against operational losses in fund management and broker activities. This is the…

Credit model evaluation

With the new Basel Capital Accord scheduled for implementation in 2005, banks are having to evaluate the credit scoring models that will enable them to meet the minimum standards for Basel’s internal ratings-based (IRB) approach. Selecting an appropriate…

IT and staff quality seen as key as India adopts Basel II

CALCUTTA, INDIA - The need to improve staff quality and use information technology (IT) effectively are among key targets for the Indian banking system as it prepares to meet intern ational standards of risk-based regulation, India’s central bank chief…

Risk financing might solve doubts over op risk insurance

LONDON - Combining risk transfer with risk financing might be one way of resolving regulator doubts about the use of insurance to mitigate operational risk under the proposed Basel II accord.