Options

Finite difference schemes with exact recovery of vanilla option prices

A model unifies the classic local vol and binomial trees to accurately price options

Smaller drawdowns, higher average and risk-adjusted returns for equity portfolios, using options and power-log optimization based on a behavioral model of investor preferences

The authors use a power-log utility optimization algorithm based on a behavioral model of investor preferences, along with either a call or a put option overlay, to reverse the negative skewness of monthly Standard & Poor’s 500 (S&P 500) index returns…

Ice tees up CDS options launch for November 9

Fight for CDS market share heats up as Ice begins clearing options and LCH preps CDX offering

One man’s trash is another man’s Treasury

With yields at record lows, investors are asking how much protection bonds will offer in a future crisis

Jerome Kemp on the skewed economics of clearing

Only Fed intervention prevented “a really big market disaster” during Covid, says derivatives veteran

Regulators should set ‘guidelines’ for CCP margins – Kemp

Citi’s former clearing head says CCPs are still competing on margin

FX volatilities fall on receding US election fears

Polls point to a decisive Biden win – though some worry market is being complacent

Quants tout alternative carry trades for the ‘new normal’

Low rates and flatlining yield curves leave investors seeking carry in swaps and swaptions

TSE outage throws structured notes into tailspin

Trading shutdown on October 1 disrupted observation dates for some structured products

Science friction: some tire of waiting for quantum’s leap

Use cases for new tech are piling up – from CVA to VAR. But so are the obstacles

IBA launches Sonia Ice swap rate

Test version of key benchmark is latest phase in switch from Libor to sterling risk-free rate

Rates and FX exchange-traded derivatives markets cooled in Q2

Interest rate options and futures turnover halved over three months to end-June

UK banks’ rate swaps books continued to grow in Q2

Interest rate swap exposures hit £4.42 trillion

Ronin, felled prop giant, shuts up shop

Firm cancels regulatory licences; traders receiving payouts on equity stakes

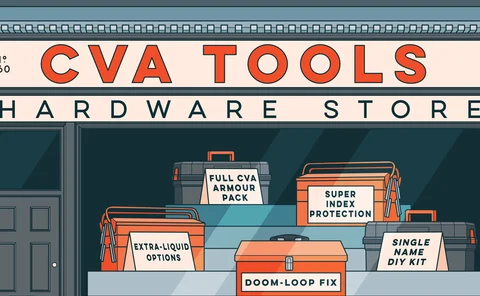

CVA desks arm themselves for the next crisis

March’s volatility forces dealers to fine-tune hedging strategies

Swaption compensation consensus proves elusive

ECB-sponsored recommendations fail to rally market behind compensation exchange solution

Swaps data: initial margin soars in Q1 2020

Model procyclicality drives wide variation in CCP IM hikes through Covid-19 volatility, writes Amir Khwaja of ClarusFT

OCC made $32bn initial margin call in Q1

Clearing house reported peak margin breach of $273 million

Bargain-hunting equity hedgers turn to FX

Currency options are cheap relative to stock index puts, but correlations are uncertain

FCMs feared systemic incident during March back-office meltdown

Trade breaks following Covid-19 spike in futures volumes required massive clean-up job, says BofA exec

Jittery ringgit spurs options growth in Malaysia

Local corporates seek new hedging tools, but longer-term options liquidity lacking

Risk doesn’t wait for market close

Many market participants rely on end-of-day batch systems to perform analytics and, in the current environment, they may see significant negative impacts on their business. Leila Sadiq, front-office risk head of product at Bloomberg, explores how the…

Structured products are lost in translation post-Libor

Benchmark shift would “fundamentally transform” popular rates structures, users fear

Managing AML and fraud – A risky business requires a risk-based approach

This webinar explores how to meet AML and fraud management obligations while empowering core businesses to remain competitive and innovative