Technical paper/Risk management

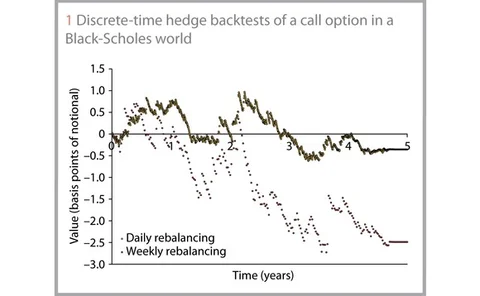

Hedge backtesting for model validation

Hedge backtesting for model validation

Exposure under systemic impact

Wrong-way risk (WWR) behaves differently for exposures to systemically important counterparties because their default has the potential to move financial markets before the close-out. Michael Pykhtin and Alexander Sokol show how the traditional exposure…

Exposure under systemic impact

Exposure under systemic impact

Longevity risk under Solvency II

Longevity risk under Solvency II

Wrong-way risk, credit and funding

The risk of exposure and counterparty default probability both increasing – so-called wrong-way risk – is usually understood in terms of the correlation between the two variables. But this approach is focused more on the centre of the distribution, and…