News/Foreign exchange

S&P alters its core earning methodology

Standard & Poor’s has reacted to criticism of its corporate rating methodology by changing its system for evaluating corporate earnings in the future. The New York-based rating agency will focus on core earnings – roughly defined as after-tax earnings…

GFI brings in leading academics for Fenics Credit

Broker and derivatives pricing software provider GFI has entered a partnership agreement with professors John Hull and Alan White, two leading derivatives academics, to develop a pricing tool for credit derivatives.

Prosecutions of Enron staff highly unlikely, says ex-employee

A senior ex-Enron employee at the heart of the scandal that led to history's largest corporate bankruptcy told RiskNews' sister publication Energy & Power Risk Management that he expects no prosecution to be brought against Enron staff.

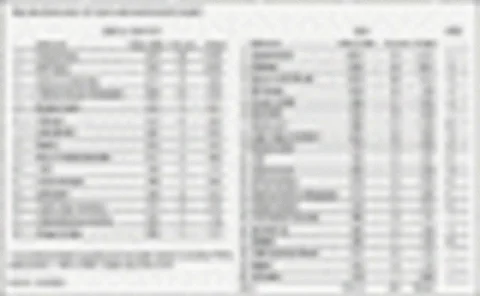

OTC derivatives volumes up 11%, says BIS

Outstanding notional volumes for the over-the-counter derivatives market stood at $111 trillion at end-December 2001 – an 11% increase from the end of June 2001, according to the latest statistics released by the Bank for International Settlements (BIS).

Risk managers leapfrog lending officers in bank hierarchy, says Greenspan

US Federal Reserve chairman Alan Greenspan said risk managers are now overtaking loan officers in the decision-making hierarchy at financial institutions, with new quantitative risk management techniques a key factor behind this transition.

Regulators to review abolition of Basel II op risk floor

Global banking regulators have asked their technical experts to look at the conditions necessary to eliminate the floor limiting gains for banks using advanced approaches to measuring operational risk under Basel II.

Rates Markets Update: Swaps see low flows with trading in narrow range

US dollar swaps continued to trade near record-low levels. Ten-year swaps ended the week at 54.5 basis points, largely unchanged from the previous Friday. Five-year spreads narrowed 8bp to 45bp. This contraction was nearly all caused by the five-year $90…

$7.3 billion in risk transferred in first index-linked synthetic CDO

JP Morgan Chase's groundbreaking index-linked synthetic collateralised debt obligation (CDO) transaction, dubbed Horizon, has transferred $7.3 billion in risk - making it one of the largest-ever synthetic CDOs. The bank had previously refused to disclose…

Park Place poised to launch Italian hedge fund

London-based hedge fund Park Place Capital plans to launch its first hedge fund in Italy. The firm, which is currently awaiting approval from the Italian regulators, hopes to launch sometime later this year, said Philip Hands, a partner at the London…

Regulator exposes potential market manipulation by Enron

The Federal Energy Regulatory Commission (Ferc) has requested that energy firms supply detailed trading data to ascertain if there was any market manipulation during the California energy crisis of 2000-2001.

No “new role” for RCC in Japanese NPL clean-up, claims ING

The decision by Mitsubishi Tokyo Financial (MTFG) to step up its sell-off of bad loans to the Resolution and Collection Corporation (RCC) will have little tangible effect on cleaning up Japanese financial institutions’ burgeoning non-performing loans …

FrontPoint hires equity arbitrage strategy team

US investment management firm FrontPoint Partners has hired a three-man quantitative equity arbitrage team aimed at developing an investment strategy generating low volatility absolute returns using liquid and risk-controlled methodologies.

FX volatility drought clears as US dollar softens

The volatility drought in the forex markets could be over, market participants told RiskNews ' sister publication FX Week , as sustained losses in the US dollar last week brought currency pairs out of the narrow ranges they have traded since the start of…

Morgan Stanley set to launch European synthetic ‘Tracer’

Morgan Stanley plans to launch a synthetic version of its tradable custodial receipt – ‘Tracer’ – product soon in Europe, following its introduction of a Tracer index based on single-name credit default swaps in the US in mid-April, and its launch of…

BofA highlights danger of over-leveraged synthetics

The over-leveraging of investment grade corporate credit-backed synthetic collateralised debt obligations (CDOs) accentuated the impact of credit downgrades last year, according to new research by Bank of America.

Rates Markets Update: Swap flows increase on economic news

Dollar-swaps saw big flows this week following a US Treasury announcement on Monday that it plans to borrow $120 billion to cover its budget shortfall. Ten-year swap spreads had come in from 57.5 basis points at the start of the week to 52bp midweek,…

Hedge funds of funds may offer CDO opportunity, says S&P

Standard & Poor’s (S&P) today predicted that collateralised debt obligations (CDOs) of hedge fund of funds will be the next sector to fuel growth in alternative investments.

Moody’s highlights swap risks within European securitisations

Using fixed amortisation schedule swaps to hedge securitisations can actually increase, rather than reduce the market risk, claims Moody’s Investors Service.

iBoxx launches Xavex

News

Swiss Re executes $40 million catastrophe risk CDO

Swiss Re Capital Markets Corporation (SRCMC) has executed what is believed to be the first ever synthetic CDO based on natural catastrophe risks. The underlying risk exposures were accessed through industry loss warranties (ILWs), for which Judith…

San Paolo plans to launch first Italian single-manager hedge fund

Obiettivo SGR, a subsidiary of Italian banking organisation San Paolo IMI, plans to become the first single-manager hedge fund launched in Italy.

AngloGold cuts hedging by 12%

South Africa’s largest gold producer, AngloGold, reduced its hedge book by 12% in the first quarter, as it moved to gain exposure to a rising spot price.

WorldCom spreads blow out

The cost of protection on WorldCom’s five-year debt blew out today, following the resignation of chief executive Bernard Ebbers.