Smart beta managers face fixed-income paradox

The extension of smart beta ideas to fixed income is posing questions about how well risk factors are really understood

Need to know

- Asset managers have sought to apply factor-based strategies to fixed income in recent years after the success of smart beta in equities.

- Though premia seen as accompanying certain factors in stocks – such as price momentum, for example – appear to exist also in fixed income, academics have struggled to explain why.

- In the absence of any consensus theory, asset managers have taken ad hoc approaches to developing products.

- Key challenges are managing the additional risks in fixed-income portfolios such as duration, and identifying suitable ways to identify securities with exposure to a given factor.

- “It is good news and bad news,” says one finance professor. “The same factors work. But it proves we don’t really understand the factors at all.”

Encouraged by the popularity of smart beta investing in equities and struggling with low bond yields, fund managers have started asking how they can extend smart beta ideas to fixed income.

It’s been slow going, so far; not least because the search for answers has raised new questions, including about the theoretical ground on which factor-based investing stands.

Strategies that return a premium in equities, such as buying stocks with positive price momentum or low price-to-book ratios, seem to work in fixed income too. But fund managers are finding the explanations given for their success in stocks fail to make sense for bonds.

“It is good news and bad news,” says Riccardo Rebonato, professor of finance at Edhec Business School and a member of the Edhec-Risk Institute in London. “The same factors work. But it proves we don’t really understand the factors at all.”

In response, academics have shifted their focus from analysing factors in specific asset classes towards seeking a unified theory that applies across all of them. That has left fund managers – in the absence of a consensus of theory – having to experiment with ad hoc approaches of their own.

The same but different

Smart beta strategies seek to benefit from the relative outperformance of stocks with specific characteristics, as observed in academic studies going back 30 years. For example, value strategies capture the excess return over time to stocks that have low prices relative to book value.

A typical factor-based strategy in equities will overweight the stocks that best represent the factor in question and underweight the least representative. In bonds, though, it is not so easy.

At the time of writing, fewer than 30 of the more than 800 smart beta exchange-traded funds listed on ETF.com’s industry database cover fixed income. Just a handful have launched each year since 2007.

There are clear ways to differentiate fixed-income securities, such as maturity dates and volatility. But most fund managers looking at the application of smart beta to fixed income concede it is harder to slice portfolios of bonds compared with stocks because a single issuer might issue multiple bonds.

“If you’re trying to run security-level analysis on fixed-income portfolios over time, even looking at just small sections of the universe, the composition of the portfolio changes by borrower, by maturity – and you have to control for all that. The upshot is there aren’t very many people who have modelling ability and knowledge to do all this effectively,” says Kate Hollis, who leads the smart beta credit team at Willis Towers Watson in London, a global advisory and broking firm.

The upshot is there aren’t very many people who have modelling ability and knowledge to do all this effectively

Kate Hollis, Willis Towers Watson

At the same time, factor-based differences in performance are less pronounced in bonds compared with equities, particularly at investment-grade level.

In theory, there could be more opportunity to harvest smart beta down the quality ladder towards sub-investment grade and high yield because correlations are lower, Hollis says. But then it becomes harder to source good-quality, constituent-level data on fixed-income indexes.

The real challenge facing asset managers, though, is how best to measure a bond’s exposure to the factor in question.

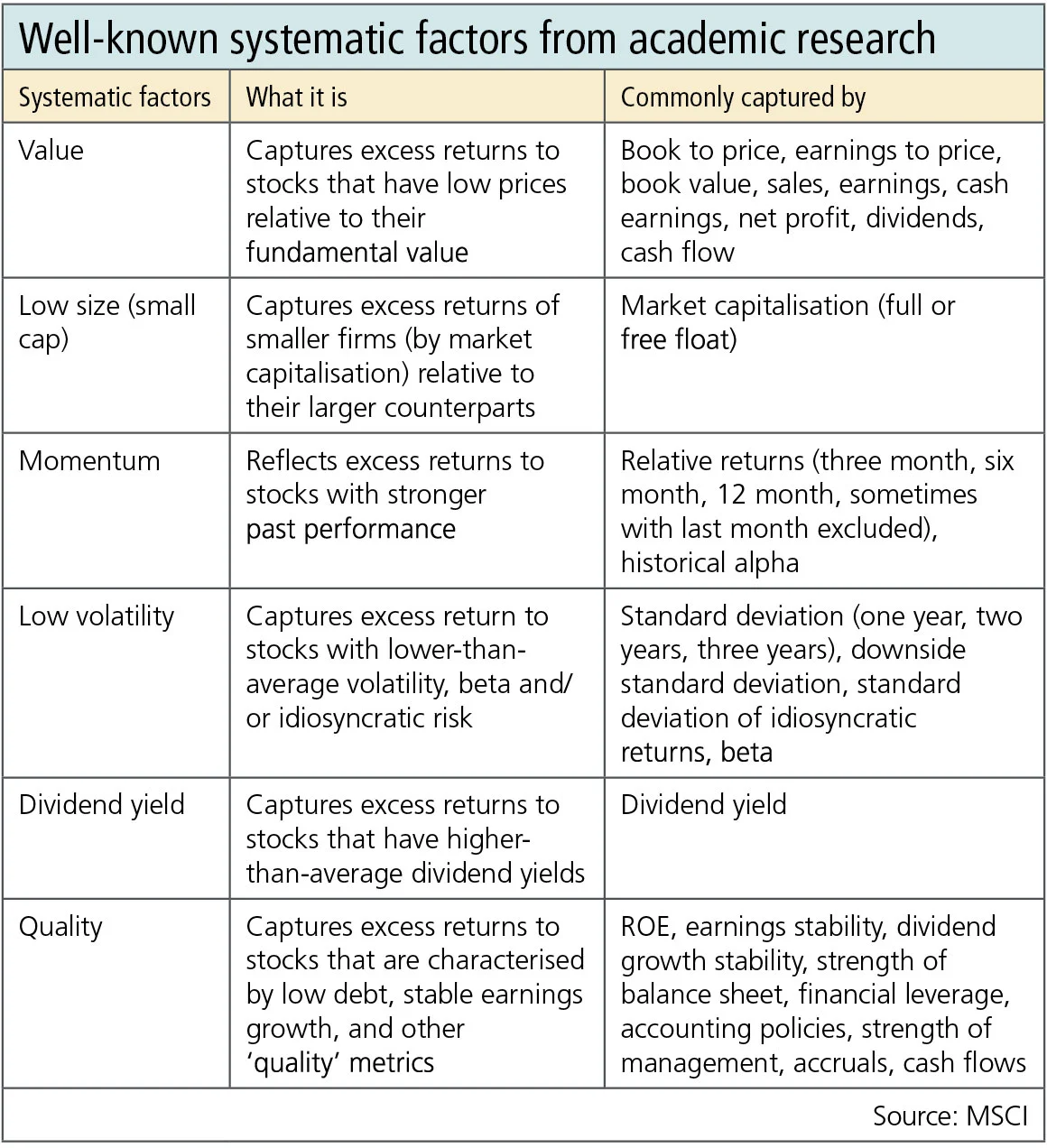

Equity smart beta funds use broadly recognised proxies to do this (see table). For value, for instance, the typical proxy in equities is the ratio of price to book value. That makes intuitive sense for stocks. But when you move to fixed income there is no equivalent.

At present, there are as many approaches to solving such problems as firms coming up with them.

Asset manager Russell Investments, for example, uses spread value as a proxy to root out the cheapest bonds, looking at option-adjusted spreads relative to a bond’s rating category.

“We think that will outperform the whole benchmark over time. We won’t necessarily be buying down in credit. We think we’re buying mispriced bonds,” says Kelly Mainelli, director of fixed-income investments at Russell Investments in Seattle.

The firm rebalances any mismatch to the benchmark in the portfolio’s other exposures using derivatives.

“Let’s say we’re yielding more than the benchmark with credit bonds we bought that are cheaply valued, but we’re short or long duration, so now we’re off the benchmark in other factors: we use either futures or credit default swaps, depending where we’re short, to ‘true’ that smart beta back to how the benchmark is,” Mainelli says.

State Street Global Advisors, which has close to $3.8 billion of AUM in smart beta fixed-income strategies, has come up with its own proxy for momentum after finding the relative returns approach often used in equities did not work for bonds.

“A lot of bonds that appear to have price momentum often are not very liquid and are not trading much. When they do trade, it leads to apparent momentum,” says Riti Samanta, global head of systematic fixed income and senior portfolio manager, in fixed income, cash and currency at SSGA.

To get around this, State Street has incorporated proxies for liquidity such as trading frequency and trading volumes into its smart beta calculations.

Liquid alternative ETF provider IndexIQ has also found evidence of the momentum factor in fixed income, but Sal Bruno, chief investment officer, says the firm was unable to research the factor properly because of the discontinuity of pricing on individual bonds.

It’s not just an academic exercise; you actually have to harvest the benefits of momentum investing

Sal Bruno, IndexIQ

At the same time, liquidity in individual bonds would be too low to support the necessary turnover in any strategy, he thinks: “It’s not just an academic exercise; you actually have to harvest the benefits of momentum investing.”

IndexIQ dropped its research in single bonds last year and turned to bond ETFs where there is far greater secondary market liquidity. The fund has since launched two fixed-income momentum ETFs with approaching $300 million invested to date.

“The target excess total return over the aggregate bond universe is 75–100 basis points, which isn’t a huge amount in equities,” Bruno says. “But in the fixed-income world, if you can do that with lower tracking error and similar volatility to the broad aggregate universe, it could be very interesting.”

Theory of everything

These three examples illustrate just some of the hoops asset managers are being forced to jump through as they extend smart beta to the realm of fixed income.

But, while assets managers seek ways to translate what works for stocks to bonds, academics are retracing their steps and looking for a single theory to make sense of observations across asset classes.

Broadly, two explanations are given to explain premia associated with specific equity factors: either investors are being compensated for extra risk – low-value stocks will sell off more sharply in a crisis, say – or markets are irrationally underpricing stocks with certain factor exposures in some way.

The problem is, when the same factors are observed in other asset classes, these explanations are not transferable.

In a 2013 paper, Value and momentum everywhere, AQR founder Cliff Asness and others sought to extend the theory of value and momentum to other asset classes. They found value and momentum returned a premium across eight markets and asset classes.

But the paper concluded this was difficult to explain using existing theories that relied on fundamental indicators such as company investment risk or company growth potential to explain the value and momentum premia. “These theories seem ill equipped to explain the same and correlated effects we find in currencies, government bonds and commodities,” the paper states.

Edhec’s Rebonato says: “The equity explanations that were [put forward] in the early studies of non capital asset pricing model factors become unconvincing when applied to completely different asset classes for which the same factors have been found to work.”

Purists argue that without a sound academic grounding and a principled approach to factor definition there is a danger the extension of smart beta to fixed income descends into a fishing expedition for factors, with firms chasing the latest fad rather than building a robust understanding of how factors behave.

Since the publication of Asness’s paper, there have been further papers looking at factors in fixed income and other asset classes, but they have been written by practitioners and have tended to focus on certain bond types and factors rather than seek an overarching theory of factors.

As a result there has been no convincing academic breakthrough.

The reason, according to Rebonato, is that academics lack access to the costly fixed-income market data they need, while banks and asset managers that have that information lack the inclination or time to carry out such research.

To remedy this, academics, banks and asset manangers should work together to carry out a “dispassionate analysis of what’s behind the data”, he says.

Until then, applying risk premia investing in fixed income seems likely to remain a fragmented exercise.

Only users who have a paid subscription or are part of a corporate subscription are able to print or copy content.

To access these options, along with all other subscription benefits, please contact info@risk.net or view our subscription options here: http://subscriptions.risk.net/subscribe

You are currently unable to print this content. Please contact info@risk.net to find out more.

You are currently unable to copy this content. Please contact info@risk.net to find out more.

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@risk.net

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@risk.net

More on Asset management

Execs can game sentiment engines, but can they fool LLMs?

Quants are firing up large language models to cut through corporate blather

Pension schemes prep facilities to ‘repo’ fund units

Schroders, State Street and Cardano plan new way to shore up pension portfolios against repeat of 2022 gilt crisis

Fears of runaway risk on offshore reinsurance

Life insurers catch the eye of UK regulator for pension buyout financing trick

Hot topic: SEC climate disclosure rule divides industry

Proposal likely to flounder on First Amendment concerns, lawyers believe

‘Brace, brace’: quants say soft landing is unlikely

Investors should prepare for sticky inflation and volatile asset prices as central banks grapple with turning rates cycle

Trend following struggles to return to vogue

Macro outlook for trend appears to be favourable, but 2023’s performance flop gives would-be investors pause for thought

Start-up bond platform OpenYield prepares to launch

Start-up aims to give retail brokers the same electronic liquidity used by the professionals

Can machine learning help predict recessions? Not really

Artificial intelligence models stumble on noisy data and lack of interpretability