Risk magazine/Technical paper

Cutting edge intro: CDOs and the risk of risk aversion

New analysis shows CDOs can withstand high levels of correlation – what they can’t cope with, though, is a sudden change in risk appetite

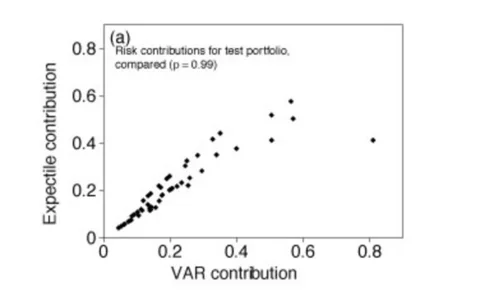

Expectiles behave as expected

Expectiles' results are analogous to those of value-at-risk and expected shortfall

Credit goes to forward rate spreads

Term structure of interest rates explained with a credit model

Why CDOs work

Collateralised debt obligations have largely gone under the radar since the 2007 financial meltdown, when their market collapsed. Nearly every attempt at explaining the cause of their failure pointed towards flawed assumptions in pricing models and…

Smile transformation for price prediction

Prediction of arbitrage-free option prices that outperform existing models

Portfolio construction and systematic trading with factor entropy pooling

Construction of large portfolios consistent with investors' views and stress test scenarios is a challenging task, considering the volume of information to be processed. Attilio Meucci, David Ardia and Marcello Colasante introduce a technique that…

Trading strategies via book imbalance

Predicting equity and futures tick by tick price movements

Regulatory-optimal funding

A treasury viewpoint on the funding optimization problem

Options for collateral options

Options for collateral options

The simple link from default to LGD

The simple link from default to LGD

Cutting Edge introduction: living la vida local

Living la vida local

Local correlation families

Local correlation families

Cutting Edge introduction: another FVA?

Including funding costs and benefits in derivatives prices is a controversial topic, closely tied up with the credit and debit valuation adjustments of counterparty risk. But new research suggests that, even with no default risk, differences in the…

SABR symmetry

SABR symmetry

Differential rates, differential prices

Differential rates, differential prices

Cutting Edge 2013: fixing SABR

Fixing SABR

Cutting Edge introduction: fixing FVA

The funding valuation adjustment (FVA) is the biggest controversy of recent times in quantitative finance. Now the authors of the original FVA paper are back – and think there may be a solution. Laurie Carver introduces this month’s technical articles

Funding strategies, funding costs

Funding strategies, funding costs

Time for a timer

Time for a timer

Cutting Edge introduction: systematic systematic factor models

Credit factor models tend to obscure the economics in favour of tractability – and this puts them at odds with rigorous arbitrage-free martingale pricing methods. To resolve this, quants are looking more closely at what a systematic risk factor actually…

Systematic risk factors redefined

Systematic risk factors redefined

Stuck with collateral

Stuck with collateral

Exchange-traded fund pair-trading strategies using autocorrelation-based mean reversion

ETF pair-trading strategies using autocorrelation-based mean reversion

Cutting Edge introduction: pricing the CVA doom loop

Pricing the CVA doom loop