Technical paper/Technology

A matter of principal

Developing term structure models can be tricky, as unknown factors and non-observable variables can affect futures prices. But principal components analysis is useful in tackling these problems. Here, Delphine Lautier uses PCA to pin down price movements…

Bond execution models

Quantitative trading l Cutting edge

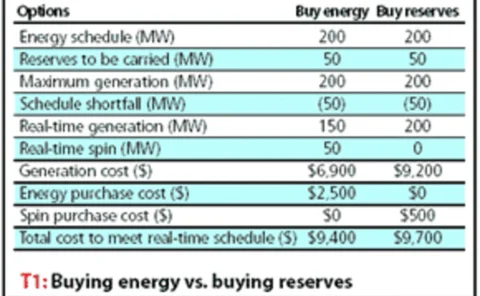

Real-time trading

Rankings 2005

Caring competition

What are the theoretical consequences of restructuring electricity markets on emissions? Here, Benoît Sévi shows that changes in supply and consumption and restructuring for competition has environmental effects, and argues that strong public policies…

Quantifying operational risk

This is the fifth of Charles Smithson's latest series of Class Notes, which will run in alternate issues of Risk through to the end of 2004. Class Notes is an educational series, designed to pull together the threads of recent developments and thinking…

An integrated framework for the governance of companies

Cases of insolvencies, losses and internal frauds have been increasing of late. As a result, the question is asked more and more often whether such cases could have been avoided with better governance of companies or a clearer organisational handbook. In…

Constructing an operational event database

Michael Haubenstock of US bank Capital One outlines a framework for an event database, formulated with current US regulatory guidance on the subject in mind. The text is an abstract from The Basel Handbook, which has just been published by Risk Books.

The score for credit

Jorge Sobehart and Sean Keenan discuss the benefits and limitations of model performance measures for default and credit spread prediction, and highlight several common pitfalls in the model comparison found in the literature and vendor documentation. To…

Trading techniques

Rankings 2004

Mark up the scorecard

Sergio Scandizzo and Roberto Setola explore the application of a scorecard approach to the measurement of operational risk, assessing both its reliability as a risk-management tool and the practicalities of its implementation.

Advancing op risk management using Japanese banking experience

Junji Hiwatashi and Hiroshi Ashida of the Bank of Japan outline a practical framework for operational risk management, derived from research and experiences in Japan's financial community.

Risk management based on stochastic volatility

Risk management approaches that do not incorporate randomly changing volatility tend to under- or overestimate the risk, depending on current market conditions. We show how some popular stochastic volatility models in combination with the hyperbolic…

Op risk modelling for extremes

Part 2: Statistical methods In this second of two articles, Rodney Coleman, of Imperial College London, continues his demonstration of the uncertainty in measuring operational risk from small samples of loss data.

Fallacies about the effects of market risk management systems

This paper takes another look at allegations that risk management systems have contributed to increased volatility in financial markets, with the particular example of the summer of 1998. The paper also provides new evidence on the potential effect of…

Credit model evaluation

With the new Basel Capital Accord scheduled for implementation in 2005, banks are having to evaluate the credit scoring models that will enable them to meet the minimum standards for Basel’s internal ratings-based (IRB) approach. Selecting an appropriate…

Linear, yet attractive, Contour

Banks’ Potential Future Exposure models are at the core of the advanced EAD (Exposure At Default) approach to capital requirements for credit risk considered in the New Basel Capital Accord. Juan Cárdenas, Emmanuel Fruchard and Jean-François Picron look…

Pro-cyclicality in the new Basel Accord

Could Basel II worsen recessions? By backtesting the proposed capital rules to the last recession, D. Wilson Ervin and Tom Wilde argue that the increased risk sensitivity of loan portfolio regulatory capital in the new Accord could have unwelcome…