Technical paper/Risk management/Risk management

Systemic risks in CCP networks

Barker, Dickinson, Lipton and Virmani propose a credit and liquidity risk model for CCPs

‘Hot-start’ initialisation of the Heston model

Serguei Mechkov initialises Heston model’s parameters using probability distributions

Adjusting VAR to correct sample volatility bias

David Frank proposes an adjustment to sample variance for the computation of value-at-risk

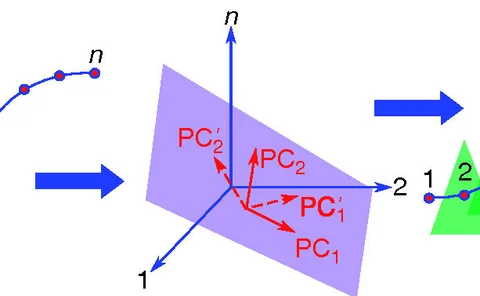

Flylets and invariant risk metrics

Kharen Musaelian, Santhanam Nagarajan and Dario Villani show how to build robust risk metrics for bond returns

Organising the allocation

Yadong Li, Marco Naldi, Jeffrey Nisen and Yixi Shi propose a new capital allocation method

Operational risk modelled analytically II: classification invariance

In a simple model, Vivien Brunel establishes the properties of an operational risk model under the requirement of classification invariance

Loan classification under IFRS 9

Vivien Brunel proposes a method to classify non-defaulted loans in accordance with IFRS 9

Expected shortfall and VAR: cracking the marginal allocations

A new method to estimate marginal VAR and marginal ES is presented

Hedging error measurement for imperfect strategies

Jack Baczynski, Jonathan da Silva and Rosalino Junior present an index for measuring hedging errors

Expected shortfall is jointly elicitable with value-at-risk: implications for backtesting

Fissler, Ziegel and Gneiting investigate the role of elicitability in backtesting problems and show how comparative backtests can be implemented for expected shortfall

Diversification benefit of operational risk

Torresetti and Le Pera explore the relevance of the diversification benefit from a theoretical and practical viewpoint

Isolating a risk premium on the volatility of volatility

Lorenzo Ravagli shows how to exploit a risk premium embedded in the vol of vol in out-of-the-money options

CVA with Greeks and AAD

Reghai, Kettani and Messaoud present new technique to calculate CVA using adjoints

Risk budgeting and diversification based on optimised uncorrelated factors

Meucci, Santangelo and Deguest introduce a risk decomposition method based on minimum-torsion bets

Jumping with default: wrong-way risk modelling for CVA

Fabio Mercurio and Minqiang Li investigate CVAs in the presence of wrong-way risk

FVA for general instruments

Alexander Antonov, Bianchetti and Mihai develop a universal and efficient approach to numerical FVA calculation

Optimal investment: bounds and heuristics

The authors present a technique for finding upper bounds on the value of a portfolio in a (possibly high-dimensional) optimal investment problem.

Outsourcing risk: a separate operational risk category?

This paper identifies three steps in sourcing risk.

Regulatory and supervisory deference in the context of Australia’s over-the-counter derivative trade reporting and derivative trade repositories regimes

This paper provides an Australian regulatory perspective on the over-the-counter landscape and shows how regulatory deference can play a facilitating role in the cross-border context.

Central counterparties: addressing their too-important-to-fail nature

This paper argues that the current international policy measures with respect to central counterparties (CCPs) only partly address the systemic risk posed by CCPs.

Analysis of risk factors in the Korean repo market based on US and European repo market experiences during the global financial crisis

This paper evaluates the Korean repo market in the light of the global financial crisis.

Banknote printing in a less-cash society: innovate or not?

Leo Van Hove investigates a less-cash society from the perspective of a central bank

Credit risk: taking fluctuating asset correlations into account

This paper puts forward an ensemble approach for asset correlations.

Wrong-way risk done right

Jacky Lee and Luca Capriotti present an arbitrage-free valuation method for counterparty exposure of credit derivates portfolios.